While You Were Debating Whether Creators Were "Real" Businesses, Visa Quietly Built Them a Bank

Visa's new partnership with TikTok isn't a product launch. It's a declaration that content creators are now a recognized class of small business and the financial world is restructuring around them

THE LEAD

There is a quiet revolution happening in the economy right now, and most business professionals have completely missed it.

Last week, Visa and TikTok launched a co-branded Creator Card in the United Kingdom — a dedicated debit card and business account built specifically for content creators. It is the first product of its kind from a major global financial institution. The headlines treated it like a tech story. It is not. This is the moment the formal financial economy — the banks, the payment networks, the institutions that decide who gets credit and who gets loans — officially recognized content creators as a new class of entrepreneur.

If you thought the creator economy was a fad, Visa just respectfully disagreed.

“The conversation has shifted from ‘Are creators legitimate?’ to ‘How do we serve them?’ That is not a small move. That is a tectonic one.”

THE DATA DUMP

Before we talk about what this means for the future, let us talk about the numbers that explain why this is happening now.

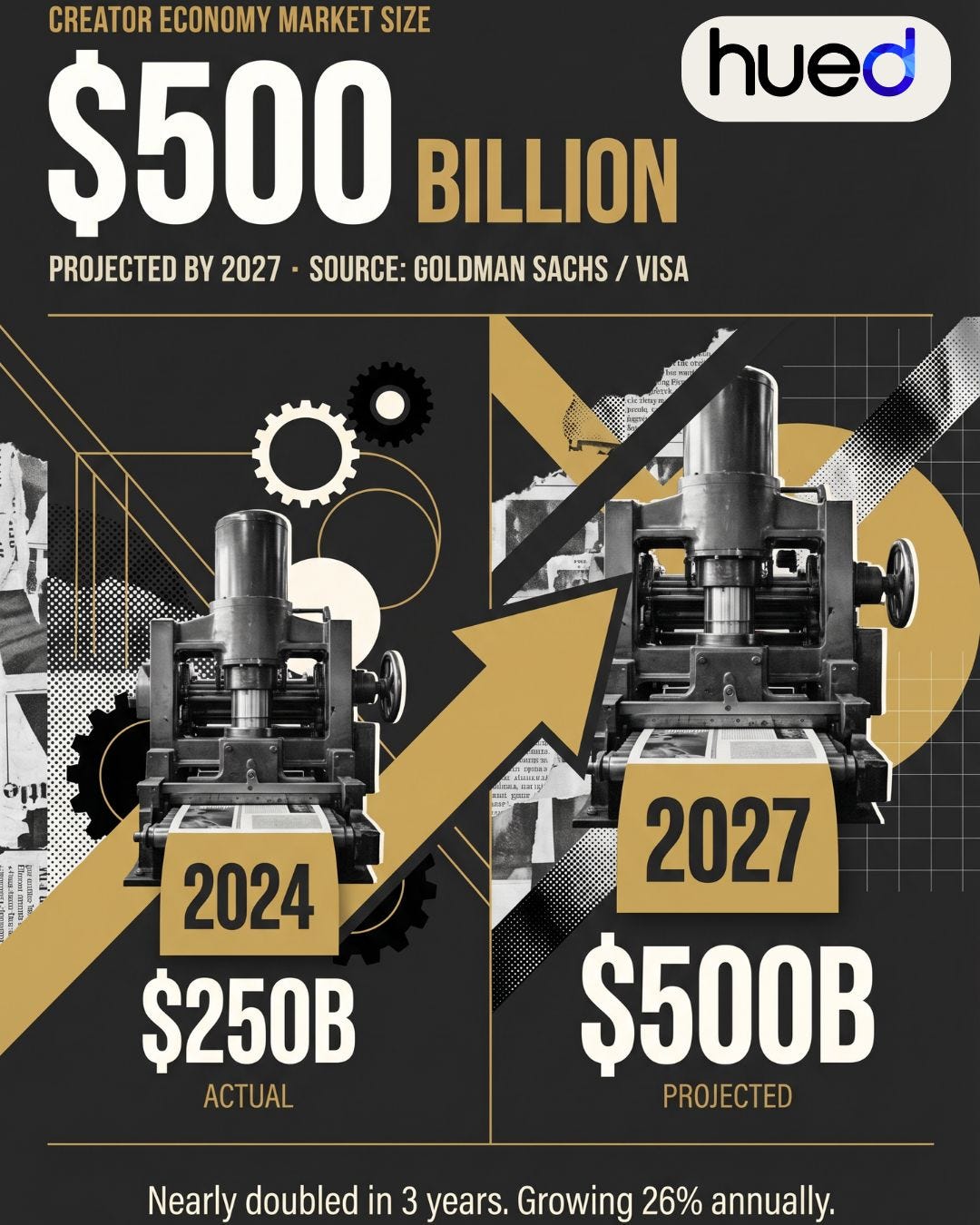

$500 Billion

Projected size of the global creator economy by 2027, up from $250 billion in 2024. (Goldman Sachs / Visa)

Think about what that means in practical terms. We are talking about a sector that is doubling in less than three years. For context, the entire US movie and entertainment industry generates roughly $95 billion annually. The creator economy is blowing past that — and it is still in its early innings.

200 Million+

Content creators worldwide — from full-time professionals to part-time earners managing multiple revenue streams. (Visa / Statista)

Two hundred million people. That is roughly two-thirds of the entire US population creating content on the internet, and a significant portion of them are earning real money doing it. Visa’s own research found that 85% of full-time creators earn up to $100,000 annually. That is not a hobby. That is a career.

86%

Of creator-run businesses are entirely self-funded — no loans, no investors, no institutional support. (Visa Research, 2026)

Here is where the story gets interesting. Despite generating billions of dollars in economic activity, the overwhelming majority of creators have been operating completely outside the traditional financial system. No business credit. No dedicated financial tools. No separation between personal and business finances. They have been building real companies with one hand tied behind their backs.

41%

Of creators have turned down new business opportunities because of cash flow problems caused by delayed or irregular payments. (Visa Research, 2026)

Let that number sit for a moment. Four out of ten content creators, meaning people with real audiences, real brand deals, and real revenue, are leaving money on the table because the financial infrastructure around them was never designed for how they work.

Income arrives in bursts.

Payments from platforms can take weeks or even months to clear.

For TikTok LIVE creators specifically, the payout process required converting virtual gifts into diamonds, then into dollars, then waiting up to 36 days for funds to settle. You cannot run a business like that.

THE STRATEGY: WHAT IS ACTUALLY HAPPENING HERE

The Creator Card solves immediate problems many creators are having: faster payouts, business-grade tools, cleaner finances. That is useful. Granted most people reading this are based in the United States and don’t see how a card only offered in the UK means something to us here.

Don’t miss the bigger story is what this signals about where the financial sector is heading.

For years, banks treated creators the way they used to treat freelancers who had unpredictable income, often thought to be too risky and therefore, not worth the product and financial services development. Getting a business loan as a creator was nearly impossible. The income documentation did not fit the standard forms. The system was not designed for someone whose revenue comes simultaneously from a platform, three brand deals, a newsletter, and a storefront.

Getting a business loan as a creator was nearly impossible. The income documentation did not fit the standard forms. The system was not designed for someone whose revenue comes simultaneously from a platform, three brand deals, a newsletter, and a storefront.

Visa is not a startup experimenting with a new audience. Visa processes trillions of dollars in transactions annually across more than 200 countries. When Visa formally classifies creators as small business enterprises (aka SMEs) in financial industry language it is not making a cultural statement. It is making an infrastructure decision. And infrastructure decisions have long tails.

“When the plumbing changes, everything built on top of it changes too. Visa just changed the plumbing.”

What comes next is predictable.

First come the basic tools such as debit cards, business accounts.

Then come credit products, think business credit lines, working capital loans.

Then come investment instruments — creator-specific funds and revenue-based financing.

We have seen this playbook with gig workers and e-commerce sellers. It always starts with a payment product and ends with a full financial ecosystem. The creator economy is at the beginning of that cycle.

WHAT THIS MEANS FOR YOU

Whether you are a content creator, a communications professional, a marketing director, or a business leader who works with creators — this shift has direct implications for how you think about the work.

If you are a creator or aspiring to become one: Start treating your content operation like a business today, before the tools fully catch up to you. Open a dedicated business account. Track your income sources separately. Document your revenue streams in a way that a bank can read. The creators who are positioned for the next wave of financial products including credit, loans, and investment will be the ones who already have their financial house in order when those products arrive.

If you lead a brand, a comms team, or a marketing department: The creator you are negotiating with today is going to be operating with a very different level of financial sophistication in the next 24 months. They will have better tools, better cash flow, and better leverage. Contracts, payment terms, and partnership structures are all going to evolve. Get ahead of it now.

If you are a business or advocacy professional who creates content: You are already operating in this space, even if you do not think of yourself as a “creator.” Every Substack, every LinkedIn article, every podcast, every YouTube channel attached to your professional brand is part of this economy. The formalization of financial tools for creators is also the formalization of tools for you.

THE BIGGER PICTURE

The internet has always rewarded attention. What is changing is that the financial system is finally building the rails to reward it with the same tools it gives every other sector of the economy.

A creator is not a hobbyist with a phone and too much free time. A creator is a media company, a brand, a distribution channel, and a direct-to-consumer retailer often all at once. The data has shown this for years. What is new is that Visa, one of the most powerful financial institutions on the planet, has now put its name on a product that says the same thing.

This is not a TikTok story. TikTok is just where it started, in the UK, with one partnership. This is a story about who gets recognized as a legitimate economic actor and what happens when 200 million of them finally do.

The shift everyone is missing is not a new platform or a new algorithm. It is a new category. And the category just got its first credit card.

THE ASK

If you are ready to stop watching this economy from the outside, subscribe at www.digitaldirectorsplaybook.com

Cameron Calvin Trimble

Your Digital Director